Mike McCaffrey

The Soul of an Agent Network

The Helix Institute has evaluated and advised all types of agent networks in countries around the world. Big ones, rural ones, new ones, bank ones, and even imaginary inactive ones. Despite the differences in operational strategies, all agent networks should have one element in common – they are crafted to deliver a value proposition to a target market.

That value proposition – the product/service that agents deliver – is the soul of the agent network. It determines the network’s optimal size, growth rate, geographical placement, agent demographics, and the level of training and support that agents receive. It is the foundation upon which all strategic operations are built.

Ironically, despite it being such a defining factor, the value proposition is rarely the issue we are asked to evaluate. Most providers feel like they have got the product right, and remain concerned with secondary issues, such as inactivity in the network, illiquid agents, or a competitor that erodes their market share. However, in our experience, those are generally indicators of larger problems.

Sitting with providers to dissect these problems, we separate the symptoms observed from the drivers that need to be addressed. We unpeel the layers of operations to find elements that have not been correctly woven into the governing strategy. Following these leads frequently guides us to the same place – a value proposition that is simply not very alluring.

An agent network will only ever be as good as the product it delivers. In digital finance, most business models need high volumes to make profits on small margins. Hence, a poor value proposition that is seldom used is going to be a perennial problem. If it does not regularly solve a key concern of the target market, it will constantly struggle to generate income for the business.

Back to the Basics of Product Development

This is not just a problem for small agent networks in the far corners of the world. It is an issue for many of the networks that we evaluate. In our latest paper, Finclusion to Fintech: Fintech Product Development for Low-income Markets, we point out that most of the formal financial products that banks and mobile network operators offer are generally not very useful for low-income people. The resultant uptake and usage speaks volumes:

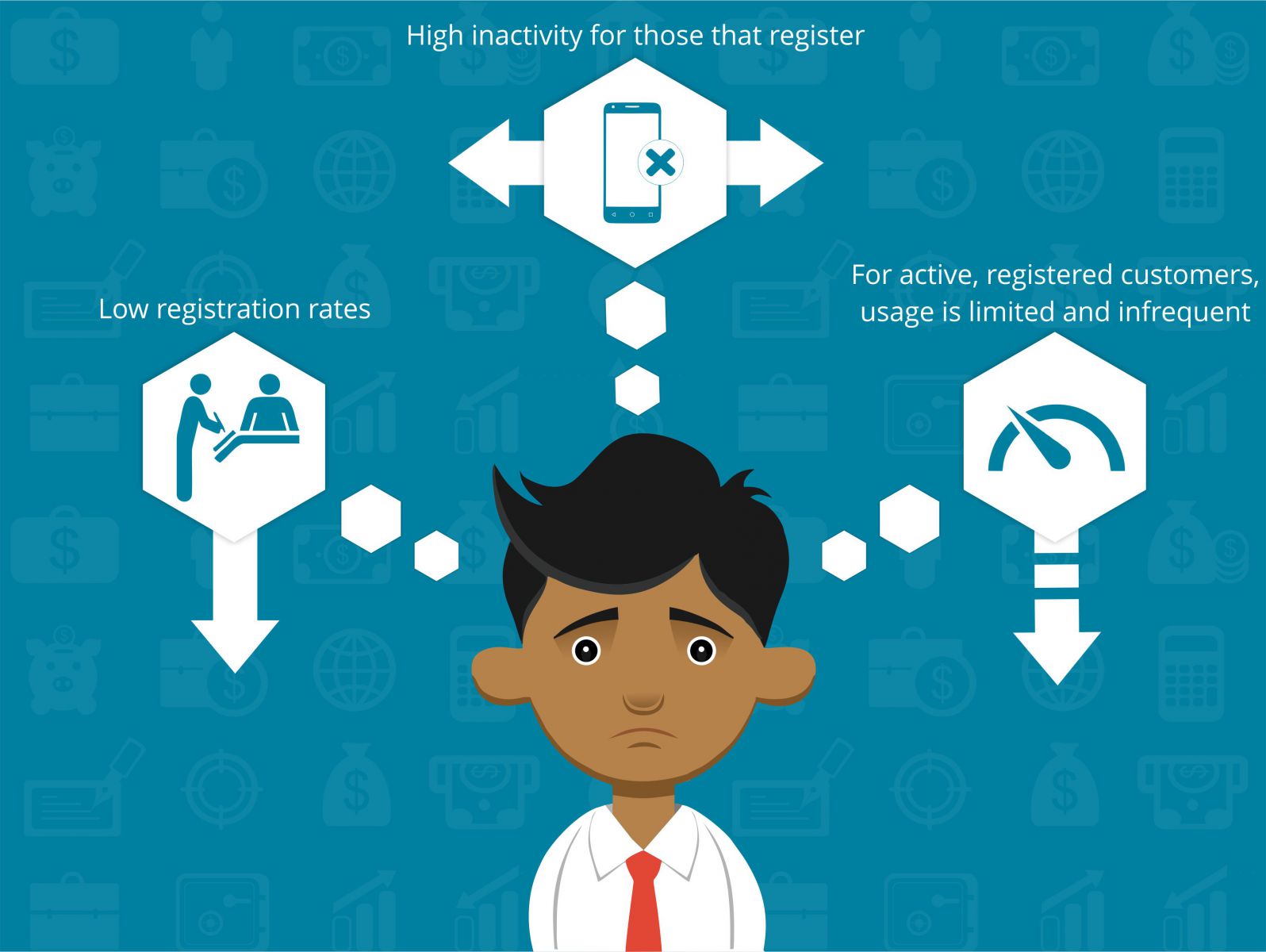

- Low Registration Rates: The GSMA 2015 State of the Industry Report states that in countries where mobile money is offered, only 10% of mobile connections are linked to mobile money accounts. The 2014 World Bank Findex data shows that only 28% of adults in low-income countries have a formal financial account (bank or mobile money).

- High Inactivity for Those That Register: The 2016 GSMA State of the Industry Report states that only 21% of registered users are active on a 30-day basis. The Making Access Possible (MAP) project studied bank account usage in six countries and found that in one country, 76% of accounts were dormant, while in the other five, 50%–71% of accounts were used as ‘mailboxes’, only to receive an occasional payment.

- For Active, Registered Customers, Usage is Limited and Infrequent: Beyond the statistics shared above on bank accounts, the GSMA 2016 State of the Industry report shares that 97% of volumes and 90.7% of values of mobile money transactions are limited to three usage cases airtime top-ups, P2P transfers, and bill pay. Moreover, the average active user only conducts 2.9 transactions per month (excluding cash-in, cash-out and airtime top-ups).

While lack of access is often touted as the key driver of the low registration rates for formal finance, the inactivity and limited, infrequent usage clearly show that the problem is much greater than just access to these services. In short, most low-income people do not register for formal finance accounts, those that do hardly use them, and those that use them, only do so for limited tasks.

Informal Foundations for Formal Solutions

What is needed is an appropriate set of tools to help people manage their money on a daily basis. Almost nothing we have seen in the market thus far comes close to this. Even when access to formal finance is extended, at best, the mass market incorporates it as yet another tool, but rarely replaces the informal systems and strategies that it uses.

In our paper, Finclusion to Fintech, we compare formal and informal financial solutions and show that the formal ones are not obviously superior as many assume they are. In addition, we review prominent financial inclusion literature and recent data from the Findex and Financial Diaries projects. These help explain why formal financial solutions are not necessarily better, and where product development needs to go to be more valuable for mass-market customers.

The expansion of agent networks across countries has been exciting, but too often the products they deliver are not. New products should avoid trying to improve upon those that people seldom use. They should be built with an understanding that low-income people have unique financial needs and ways of thinking about money management that are still not being met by formal providers. Providers should aim to improve and formalise the often risky informal financial solutions people cling to even when offered formal accounts.

This philosophy should lead the next generation of product development as fintech companies vie to reach the mass-markets of the developing world. Our latest paper is meant to serve as a proverbial Rosetta Stone, translating decades of financial inclusion research into the business opportunities they uncover for fintech innovators. By providing more value for customers, more people would use these products with increased frequency, alleviating many of the most common problems we have seen with agent networks around the world.

View the full report: Finclusion to Fintech: Fintech Product Development for Low-income Markets