Jacqueline Jumah

Irene Wagaki

Customer development is a fundamental requirement for any business. In digital financial services (DFS), we can view customer development as a journey that comprises customer discovery, customer captivation, and appropriating value. Customer discovery involves finding out about potential customers, and understanding whether existing solutions are able to meet their needs. Customer captivation entails continuously sustaining the interest of the customer by ensuring a positive user experience. Appropriating value focuses on adding valued products, services, and delivery channels that can deepen early market successes to generate revenue and thus profits.

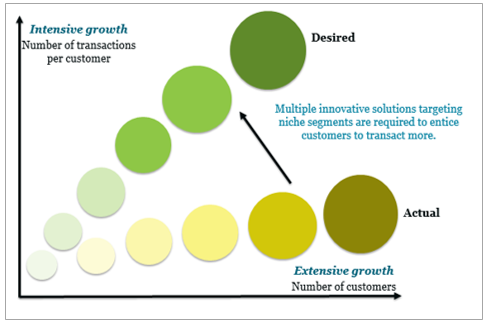

So far, in customer discovery, many financial institutions replicate solutions to drive user adoption. A few financial institutions conduct initial market research to understand the pain-points among DFS users. In customer captivation, the emphasis is on heavy marketing communication – creating awareness on the existence of different solutions. There appears to be a greater focus on the success of a transaction rather than on the user experience that drives adoption and long-term use. Providers often focus on the number of customers rather than the value per customer, which requires innovation. The adjoining diagram illustrates this:

Source: Adapted from the Open APIs in Digital Financial Services 2017 report by CGAP

Providers lose out on profitability by failing to optimise the customer value proposition that drives adoption, and in their inability to support this through the creation of appropriate mission-oriented structures. Examples of these structures include setting out autonomous DFS departments, appropriate budget allocation, operating with adequate teams, among others.

Customer Development in Nigeria

In Nigeria, Deposit Money Banks focus on raising deposits from the public to fund the corporate sector but typically do not offer a full range of products and services to the mass market. Agent banking can promote greater access to convenient and accessible transactional services throughout the country. The agent channel can be used by providers to significantly increase customer captivation and revenue per customer. At present, the primary focus of the financial institutions that have adopted agent banking is on the customer discovery phase – primarily through offering the channel for Cash-In and Cash-Out. There are few value-added services that customers use. To drive revenue per customer, Deposit Money Banks must combat the perception that they are only used for the storage of funds. This would encourage their customers to use the products and services that ride on the agent channel.

Providers must ensure that services can meet the actual needs of customers, provide an optimal user experience, and use agents as a Below-the-Line marketing channel to demonstrate the range of services available. This is essential if the aggressive Above-the-Line (in most cases) and Through-the-Line (SMS blasts) marketing communications that Deposit Money Banks typically use are to be effective.

Beyond deposits, many mass market customers’ needs are served by Microfinance Banks that provide a better user experience. But agent banking combined with customer-centric product development and appropriate partnerships with fintech companies could extend the range of personalised retail services that Deposit Money Banks offer. This would allow them to compete with the Microfinance Banks.

How Might Institutions Harness Opportunities in Customer Development in Nigeria?

One of the research focus pillars in the recently published Agent Network Accelerator Research: Nigeria Country Report 2017 by the Helix Institute of Digital Finance has been customer development. The report outlines the need for providers to use research to generate compelling value propositions beyond cash deposits and cash withdrawals. We have identified use-cases within the payments space, including social transfers, such as from donors or government, person-to-business, for instance, payment of school fees, and person-to-person funds transfer. Designing use-cases around pain-points would drive customer adoption and thereby revenue per customer.

The survey finds that providers have been doing little to promote uptake and usage. Rather, innovative agents have themselves developed mechanisms to promote uptake and usage. Typically, these mechanisms are built around digitising locally accepted cash-management practices:

a) Providing Micro-loans to Customers

Agents offer passbooks to customers for record-keeping and use these records to provide loans to them. A good number of agents report that the act of filling up the passbooks themselves provides opportunities to interact with the customers, making them feel “special”. Agents value the customers’ body language and demeanour as additional information that is critical in the intuition-based assessment of customers for microloans – of course, in addition to the transactional patterns. The transaction sessions with customers also involve asking personal questions to unearth their financial needs. An agent reported that he would provide a higher value loan to a customer who was confident enough to share more about their personal business progress than one who provided guarded responses.

The takeaway for providers: This example shows how agents use their customer relationship and information available on the channel to reduce the risk of micro-lending. The options available to providers include lending to the agents for on-lending or adopting agents into micro-lending processes given that pure digital lending carries significant risks of non-recovery.

b) Digitising Esusu and Ajoo Using Roving Employees

Some agents employ roving staff to provide Esusu services and facilitate Ajoo services through the agent banking channel. From the Helix field interactions, agents report that considerable financial information is shared in the Ajoo meetings, and this could be helpful in product evolution to make solutions more meaningful to the daily lives of customers.

The takeaway for providers: Develop field-based applications to digitise the Esusu or Ajoo processes, thereby improving the agent business-case and enhancing agent loyalty, and through their actions increase the transaction volumes and deposits mobilised. Digital tools, such as tablets and smartphones that offer other intuitive interfaces could be used during these sessions to improve the interactions and ensure prompt data collection.

c) Facilitating Remote Transactions

Due to a lack of service reliability and limited access to liquidity experienced by agents, they have developed networks to aid in facilitating transactions remotely. This means that whenever a customer visits an agent who is unable to conduct transactions for any reason, another agent in the network conducts the transaction on that agent’s behalf. For example, a customer wants to deposit NGN 5,000 walks to an agent in his locality – agent A. Unfortunately, due to network issues, the service is unavailable and agent A is unable to conduct the transaction. Agent A then reaches out to agent B – who is in a different locality through a call. Agent A provides the customer's transaction details and agent B immediately conducts the transaction on his behalf. This is also practiced whenever there are liquidity management issues, and in both cases, the agents reconcile through their network. These agent practises follow the principles of Hawala[1].

The takeaway for providers: Providers could design products that facilitate remote transactions and the reconciliation between agents in such a way as to provide transparency on the underlying transaction to conform to Anti Money Laundering/Combating the Financing of Terrorism (AML/CFT) requirements, and to ensure consumer protection. These mechanisms could enhance services delivery, especially in rural areas where access to agent rebalancing points is a challenge.

Where is the Prize?

Providers must create value for agents and customers if they are to benefit from increased transactions and deposits. Providers would be able to increase usage through digitising local use-cases and by enhancing the user experience. This is the key takeaway from M-PESA's ‘Send money home' campaign – it mirrors existing local financial practices. In this way, providers can maximise value per customers and ultimately be able to appropriate value, which is pivotal for DFS business sustainability.

[1Hawala is a popular and informal value transfer system based not on the movement of cash, or on telegraph or computer network wire transfers between banks, but instead on the performance and honour of a huge network of money brokers known as "hawaladars".